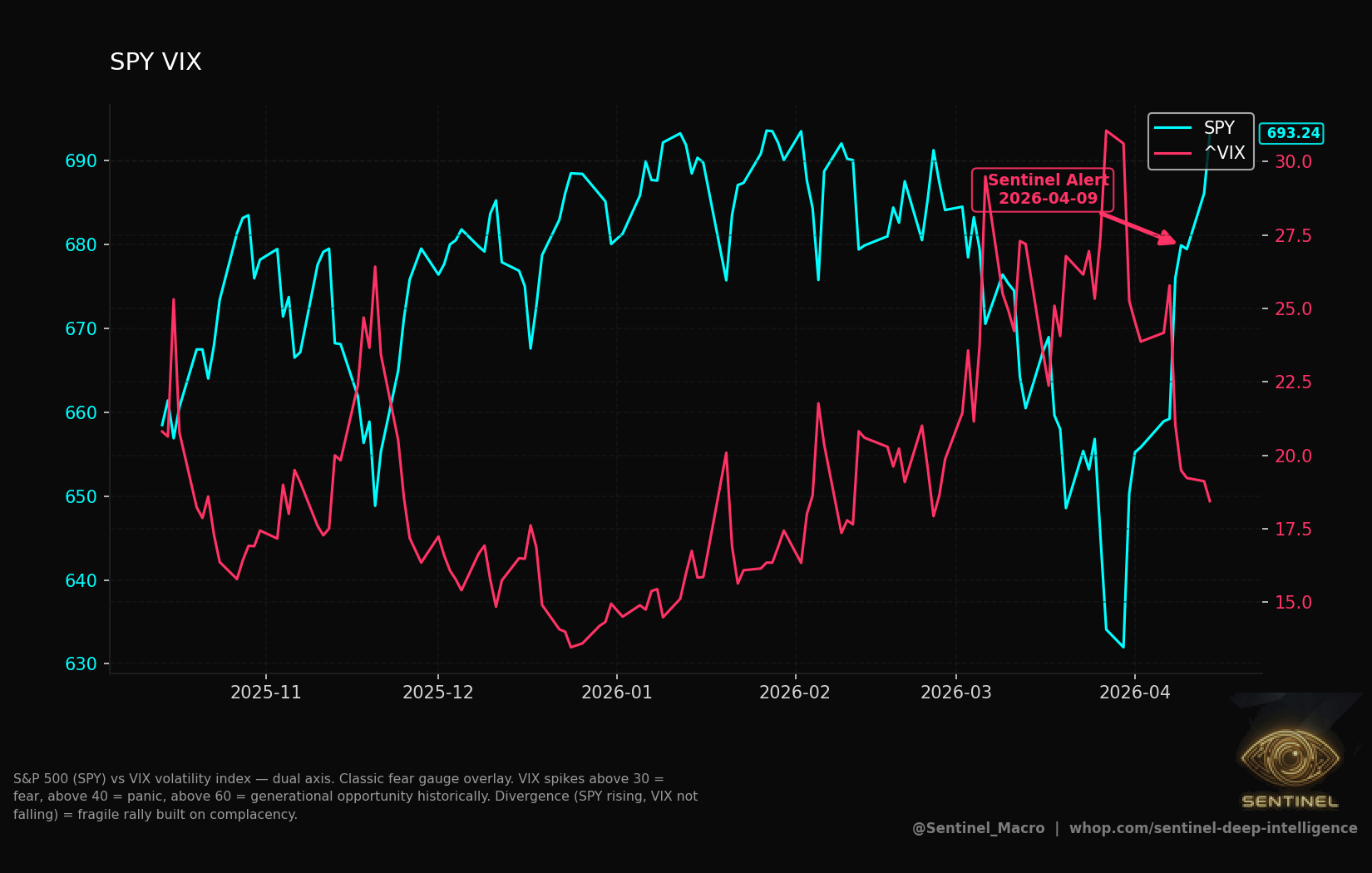

🔮 SENTINEL WEEKLY — April 9, 2026

Risk Temp: 🟡 Caution | VIX: 19.9 | F&G: 14

🐙 Reality Gap: Policy Certainty vs Headline Panic

Aha! The market’s public fear is loud, but the money with skin in the game is quietly pricing policy continuity.

- Polymarket shows near-certain Fed leadership and a June pause: Kevin Warsh 96%, and June FOMC — No change 88%. That’s real-money probability, not a soundbite.

- Options tell the retail panic story: Put/Call ~1.23 (today’s flow: puts outpace calls), while dealers’ GEX sits at $5.35B and DIX at 45.5% — institutions are net-bidders and gamma will blunt then accentuate moves.

- Headlines remain crisis-focused (Hormuz, regional strikes) and push volatility spikes. Yet breadth and flows say participation is narrow but not capitulative: Breadth 51%, equity fund inflows $40.5bn (week ending Mar 25).

Historical parallel — Playbook moment:

- April 2019 had the same split: a visible crisis narrative, but prediction markets and dark-pool prints priced policy continuity. Result: a two-week headline selloff, then a selective squeeze into safe-quality names (+6–8% sector rotation in three weeks). The mechanic then was flow, not fundamentals. Treat today the same: headline shock creates tactical windows, not regime change.

Implication: size exposure into dips and own convexity. Use volatility spikes to buy high-quality exposure, not to flip into risky breadth plays. Dealers’ gamma means intraday whipsaw can become intermediate buys; prediction markets compress the policy tail.

Narrative chart block

Polymarket Vs Vix

Polymarket Vs Vix synced from Sentinel's chart arsenal.

Narrative chart block

Darkpools Gex

Darkpools Gex synced from Sentinel's chart arsenal.

Daily breakdowns with institutional plumbing, on-chain flows, and real-time regime tracking run on the premium feed. Link in bio.